Internal control is an essential activity for all private companies and public administrations involved in managing their risks. As a cross-functional, collective approach, internal control links strategy with operations to prevent risks and protect the organization.

Alongside internal audit and compliance, internal control forms the winning trio of a high-performing organization that places the quality of its products and services at the heart of its relationship with its customers, users, and partners.

(Re)immerse yourself in the heart of internal control and explore the benefits of digitalization for effective internal control.

Internal control is a cross-functional risk management tool. It aims to monitor the effectiveness and compliance of processes, procedures, and standards implemented internally to ensure the security of the company or administration.

Internal control focuses in particular on the proper operational implementation of the risk management plan. It therefore protects the organization against fraud, human error and, more broadly, the risks to which it is exposed, in an increasingly unstable, complex, and demanding environment.

Implementing an internal control system is not a legal obligation, except for banks, finance companies, and payment institutions governed by the Monetary and Financial Code. However, it has now become essential for all companies, local authorities, and public administrations that wish to secure their activities and combine performance with quality.

As a synonym for optimized, compliant management, an internal control framework conveys to public and private customers, users, and partners an image of reliability, trust, and transparency.

The internal control function is not governed by official standards. However, it can rely on recognized frameworks, originally inspired by financial and accounting issues. Today, it is the COSO framework—stemming from the work of the Committee Of Sponsoring Organizations of the Treadway Commission—that serves as the reference for companies and public administrations.

The COSO framework sets out internal control in four main objectives:

The COSO methodology breaks down the internal control function into five components:

The internal control framework is reflected in formalized measures and procedures, applied at all levels of the organizational chart. It is therefore the responsibility of all employees, whether company staff or public administration agents.

Even if it is led by a dedicated department or a project lead, internal control must be part of a collective approach to be effective. As the operational arm of internal control, operational teams are the ones who, on a daily basis, apply the processes and procedures defined by internal control.

Whether a company employee or a public administration agent, the internal controller drives the project and is responsible for its rollout. Their role:

Internal control is carried out as part of a structured approach tailored to the organization. Cross-functional and collective, internal control requires method and a high level of rigor at every stage of the process.

Eight risk categories are generally identified within the scope of internal control: legal and regulatory compliance, finance, accounting, operations, data and information security, environmental compliance, employee health, and reputation.

Within each risk category, internal control seeks to identify the risks that threaten the objectives of the company, local authority, or administration.

Based on the risk mapping methodology, the identified risks are then classified according to their criticality. This is assessed using two objective criteria: the impact of the risk on the organization and its likelihood of occurrence. Each criterion is assigned a score on a numerical scale, using the scoring technique. Cross-referencing the results makes it possible to estimate the level of each risk.

Even when it is based on concrete and objective information, risk assessment and prioritization remain subjective. They depend on the context and robustness of each company or administration, and on the level of vulnerability each is willing to accept.

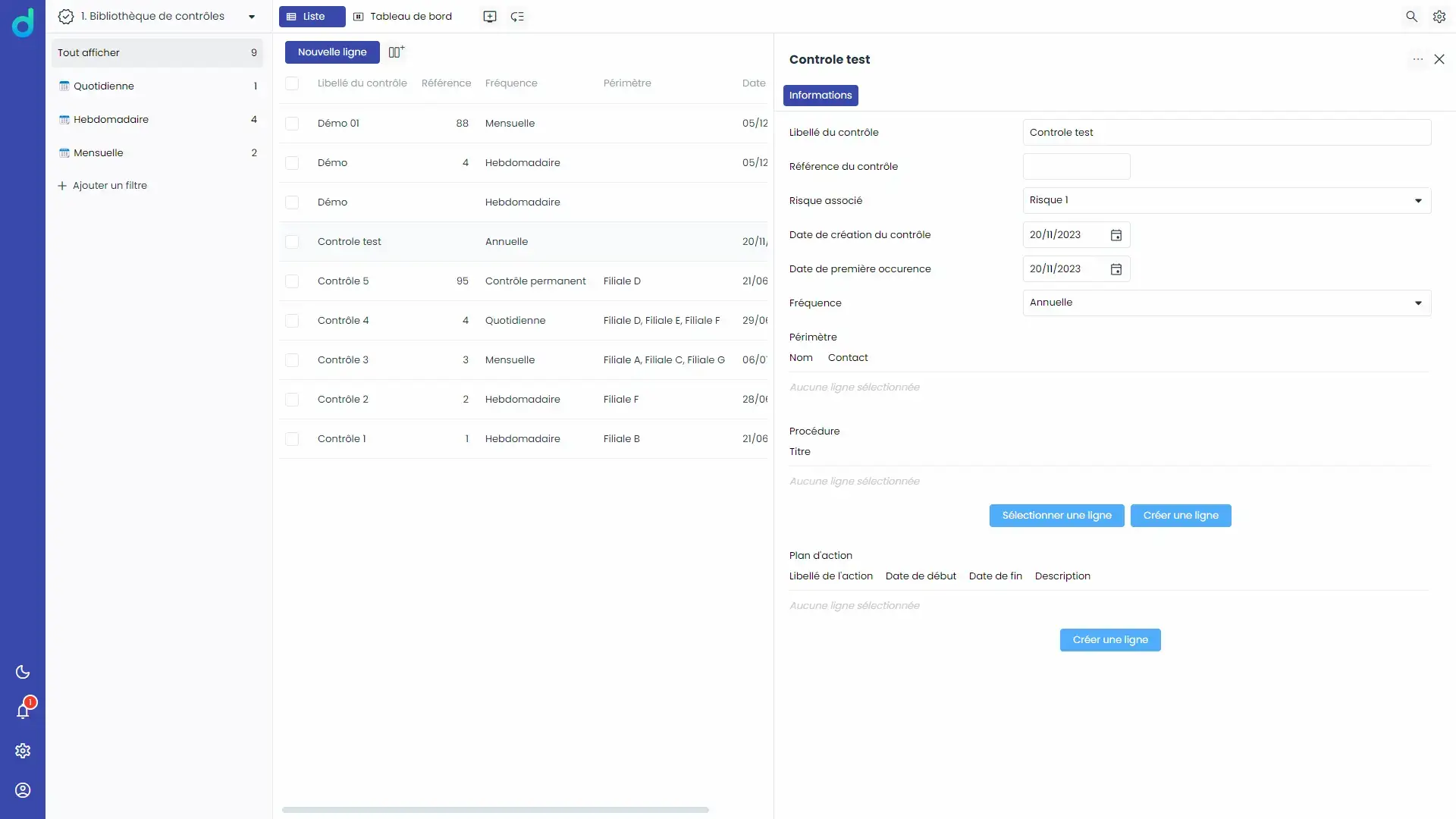

The risk assessment process results in the development of a tailored and adapted risk management plan. This plan defines, schedules, and prioritizes the control measures to be implemented, area by area, to ensure the efficiency, reliability, and compliance of operations.

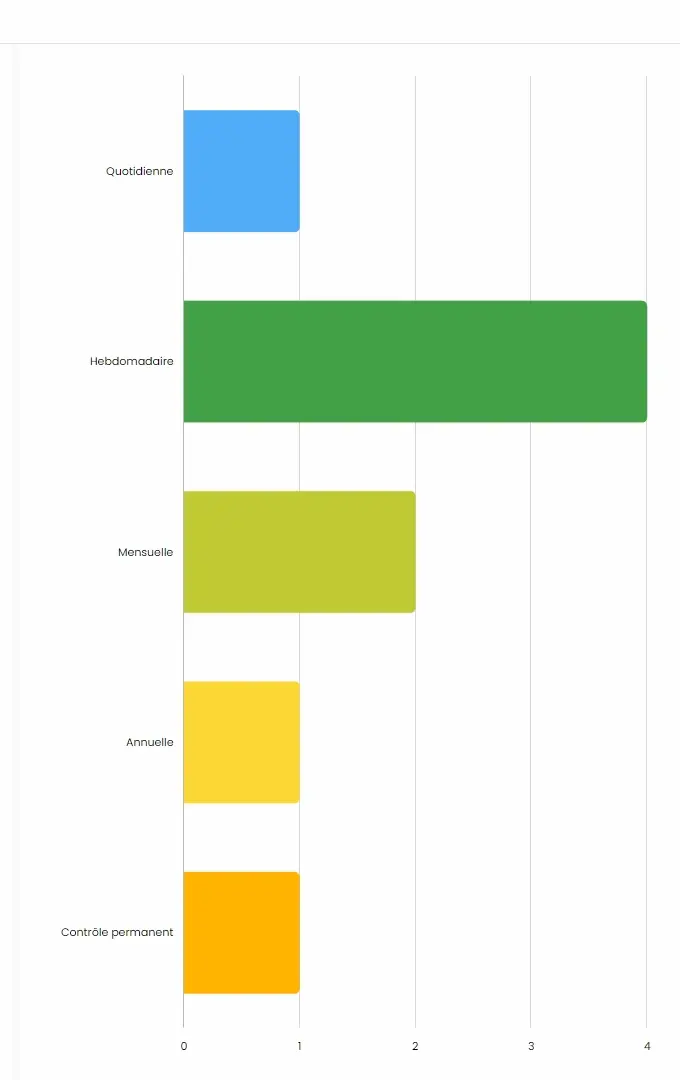

The risk management plan is rolled out across the organization, at all levels of the organizational chart. The dissemination of best practices takes the form of standardized procedures, shared frameworks, targeted regulations, tangible protection measures, flow charts, access rights, etc.

The human factor plays a crucial role in the success of this step. As it implies changes to working methods, the introduction of new procedures may meet resistance. Listening, information, communication, documentation, and training are key to mobilizing and supporting change. To secure buy-in and ensure proper application of the rules, the internal control lead must take the time to explain, clarify, and put into perspective each person’s responsibility and role in risk management.

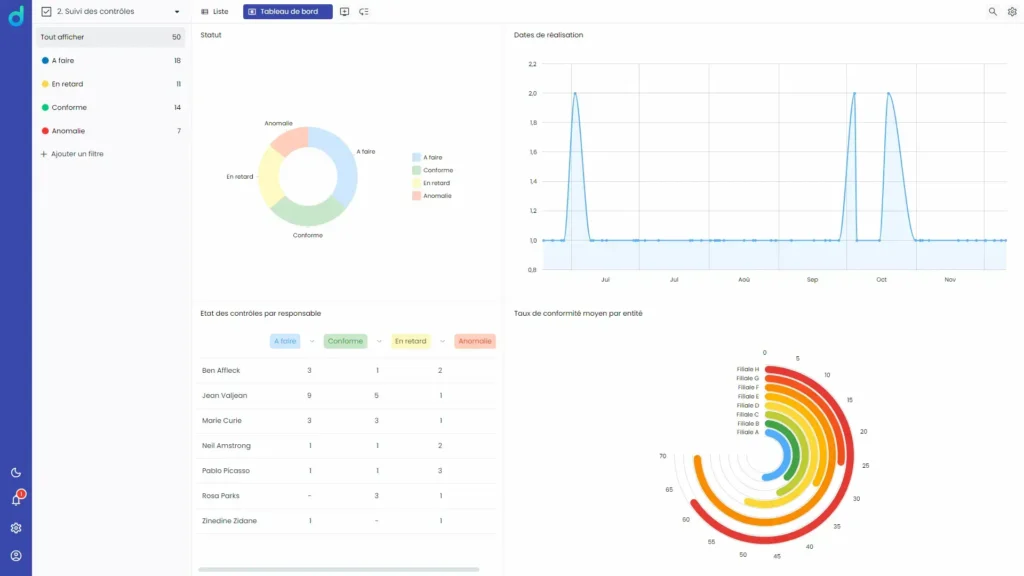

Internal control is a long-term approach. The internal control department must periodically verify the effectiveness, relevance, and proper application of risk prevention measures.

Regular “controls of controls” help identify obstacles and operational malfunctions. Listening to employees and analyzing incidents help optimize procedures, as part of a continuous improvement process for the internal control system.

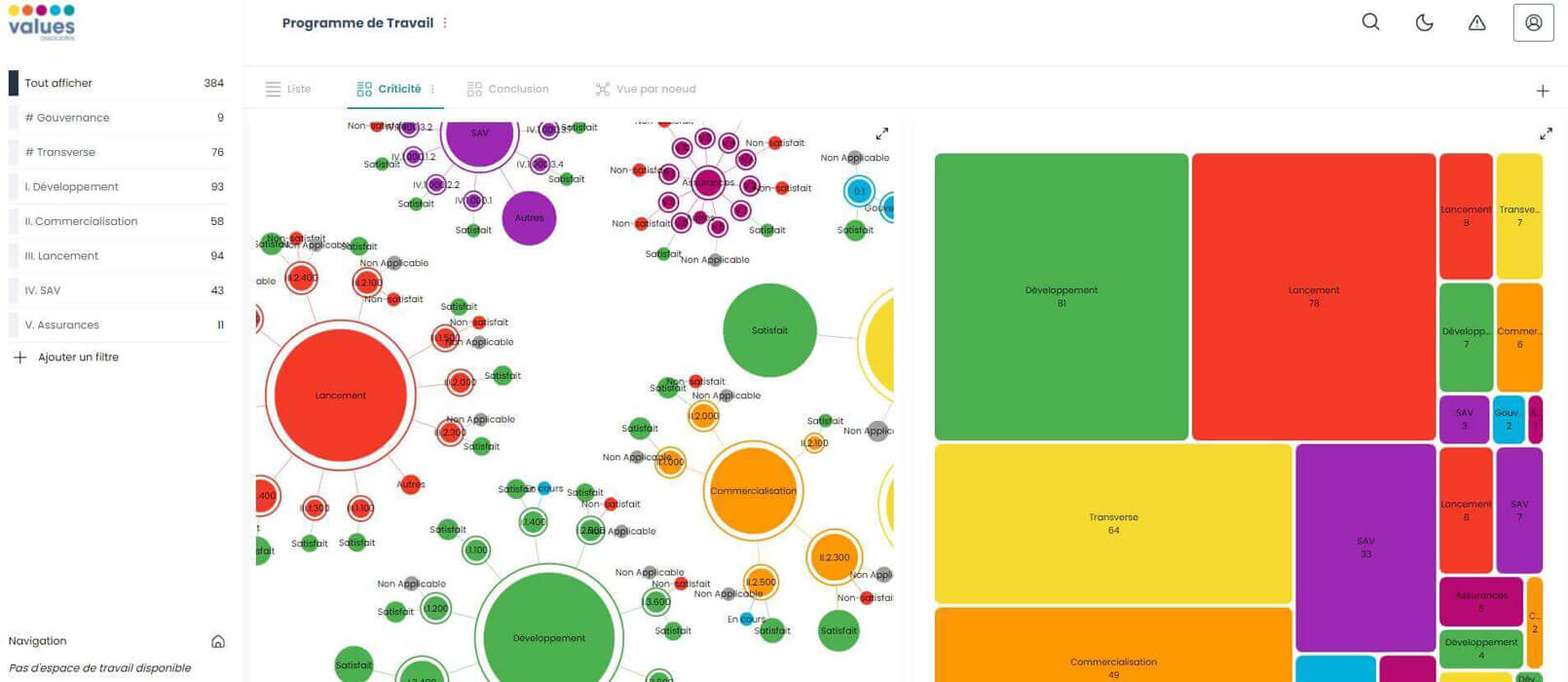

In recent years, the digitalization of internal control has become established within organizations as a lever for performance and visibility. It addresses the challenges of this global, cross-functional, and complex activity, which covers a wide range of areas and involves many employees.

Using software dedicated to internal control makes it possible to optimize and strengthen the reliability of the internal control function at every stage. With features such as automation, customization, traceability, and sharing, internal control software:

Digitalization delivers a real gain in productivity and time, both for the internal control department and for all employees involved in the internal control process.

Internal audit makes it possible to verify the effectiveness and relevance of one or more of the organization’s processes, in light of its objectives and risks.

Carried out on an ad hoc basis, this tool can be used to assess the internal control function. The audit report provides concrete information to build on the strengths of the internal control system, identify sensitive areas, and optimize practices and processes.

Thanks to this new perspective—neutral, objective, and independent—internal control can continue to improve as part of a continuous improvement approach. In this way, internal audit and internal control complement and reinforce each other, for a company, local authority, or administration that is ever more effective and secure.

Effective internal control requires following best practices in management and communication. Key success factors include:

The effectiveness of internal control relies on collective mobilization. Formalizing each person’s missions and responsibilities, as well as delegations of authority, facilitates buy-in and an effective operational implementation of internal control.

The cross-functional nature of internal control requires clear, reliable, and accessible information. The communication strategy must be deployed as soon as the decision is made to implement an internal control policy.

Its effectiveness depends on everyone’s involvement. The communication challenge is to turn internal control into a collective endeavor, where each employee is an important link in the risk management chain. It must succeed in transforming the constraint of a new procedure into a driver of individual and collective progress.

To overcome any resistance and ensure procedures and frameworks are applied consistently, appropriately, and harmonized, in compliance with the rules.

To the organization’s changing context and external developments—regulatory, social, economic, or environmental.

An effective internal control system is one of the keys to a high-performing organization with controlled risks. An internal control framework:

And for even more effective internal control, digitalize your activity with internal control software. It is the assurance of even greater productivity and performance!

Values Associates has developed software dedicated to internal control for businesses and public-sector stakeholders.

Discover our software and request a demo.