With the exception of banking institutions and insurance companies, internal audit is not a regulatory requirement. However, this activity is now essential within businesses, local authorities, and public administrations.

In a context where risks are increasingly numerous and impact all areas, internal audit is at the heart of every risk management system. (Re)discover internal audit and its challenges, as well as best practices for conducting effective audits and successfully navigating digital transition.

Internal audit is now an essential activity to ensure the effectiveness of businesses, administrations, and public institutions, and to protect them from the risks to which they are exposed.

Internal audit has an objective of assurance, evaluation, support, and advice. It allows for the assessment of the effectiveness, reliability, and compliance of all processes, procedures, and internal control systems implemented within the company or administration. In their audit report, the auditor highlights the organization’s strengths and makes recommendations to correct dysfunctions and optimize practices. The ultimate goal is continuous improvement of the organization’s quality and efficiency.

Audit analyses, observations, and reports also provide leaders and elected officials with the insights to guide policies and secure strategic decisions.

Conducting an internal audit requires rigor and the auditor’s adherence to structured steps, subject to international standards for the professional practice of internal auditing (IAAS).

Thorough preparation is essential for an effective internal audit. The first step is to define the objective, scope, reference frameworks, deliverables, and timeframe for the audit engagement.

This phase results in the definition of an audit plan, tailored to the activities and challenges of the company or administration.

Internal audit involves cross-referencing multiple data points to ensure objective results. To collect this information, the internal auditor interviews stakeholders and utilizes various tools (individual interviews, questionnaires, document reviews, on-site observations, task analysis grids, flowcharts, etc.).

At the beginning of the engagement, a kick-off meeting allows the internal auditor to explain the audit plan and methodology. It is also an opportunity to reassure stakeholders for whom "audit" might be synonymous with "inspection."

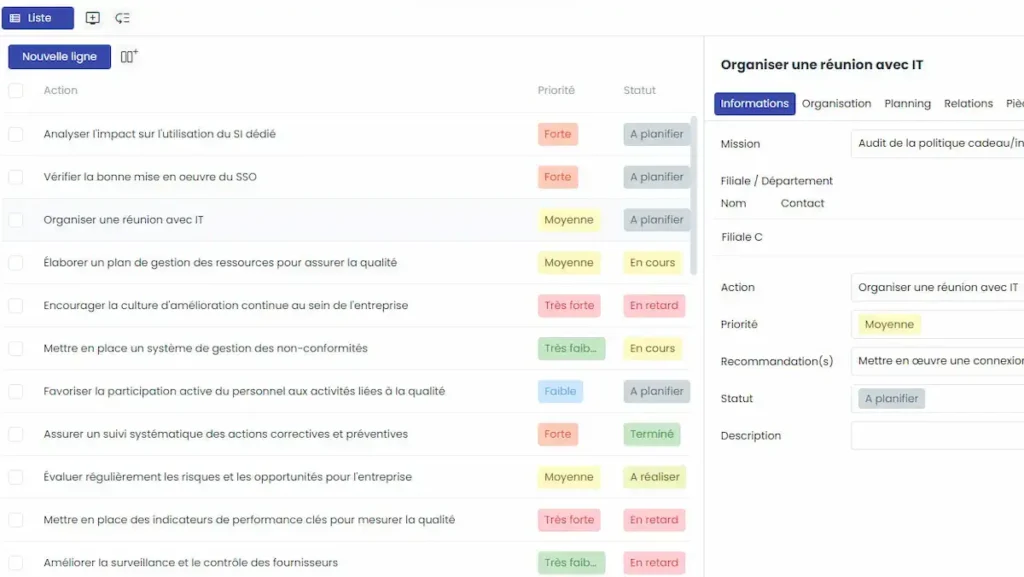

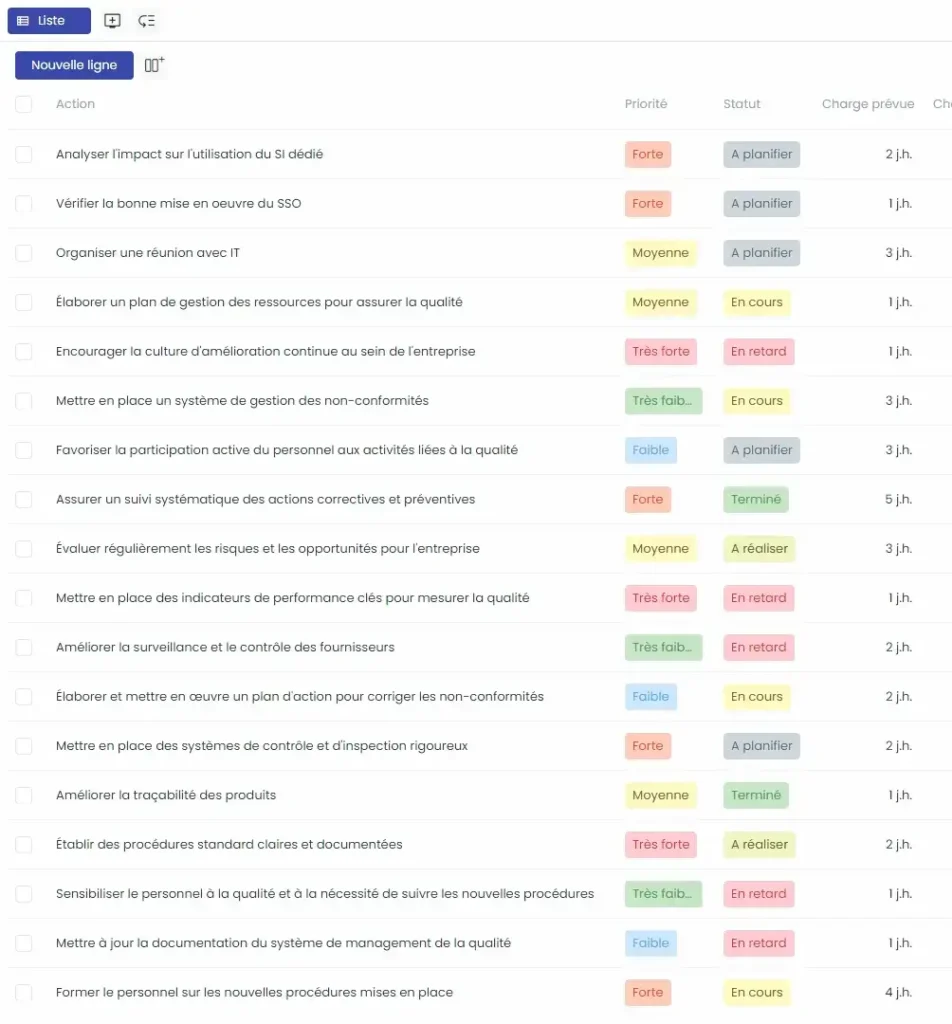

The internal audit concludes with the drafting of the audit report. The auditor's conclusions are accompanied by observations and recommendations to capitalize on strengths and improve sensitive or non-compliant areas.

Depending on the scope of their mission, the auditor may propose an action plan and monitoring indicators for the implementation of corrective actions.

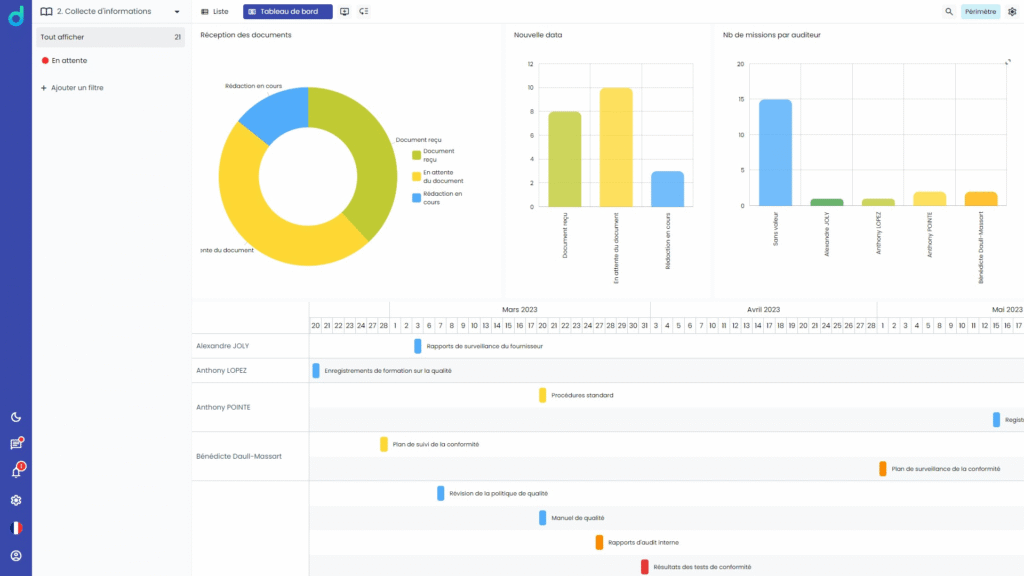

At all stages of the audit, dedicated internal audit software offers significant time and efficiency gains for the auditor. Automation, customization, sharing, and traceability features allow for:

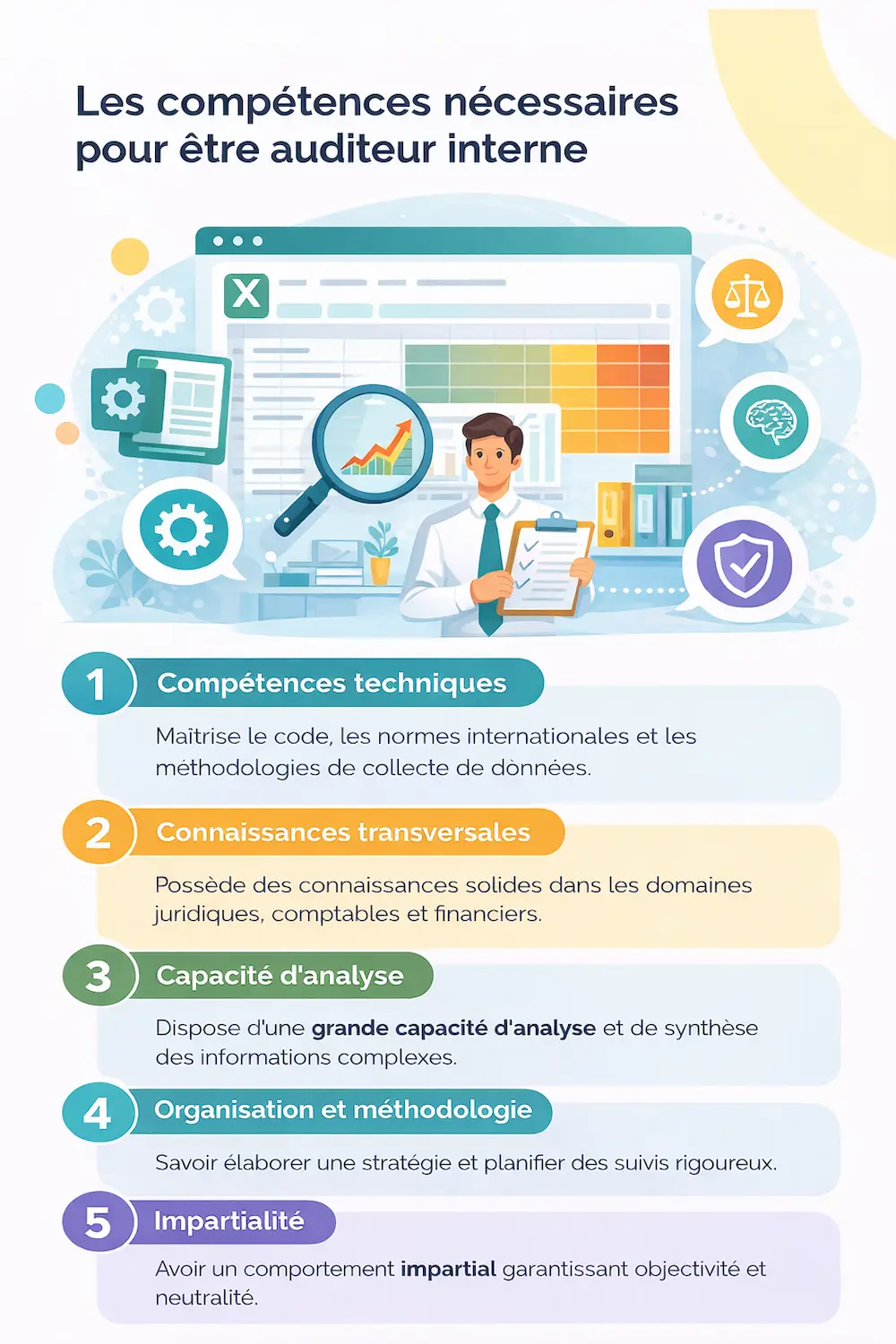

Internal audit is a demanding and responsible function. The internal auditor must combine solid technical expertise, strong analytical and organizational skills, and excellent interpersonal abilities.

A good internal auditor:

Internal audit activity contributes to improving the organization’s effectiveness, securing its governance, and enhancing decision reliability. This management tool contributes to the economic, financial, and commercial performance of the company, while protecting its assets. It supports public sector entities in arbitrating budgetary choices, analyzing the effectiveness of public policies, improving user services, and addressing public action transparency challenges.

Internal audit is also an essential risk management tool, complementing control and compliance activities.

Internal and external audits pursue different but complementary objectives.

L’objectif de l’audit interne est centré sur les processus opérationnels internes de l’entreprise, de la collectivité ou de l’institution. Il permet de vérifier le respect, l’efficacité et la conformité des procédures et contrôles en place pour maîtriser les risques. Ponctuel, l’audit interne peut être général ou cibler un processus spécifique.

L’audit interne est piloté par un collaborateur, salarié de l’entreprise ou agent de l’administration, généralement rattaché à la direction. Intégré dans une équipe d’audit dédiée ou chef de mission, l’auditeur interne maîtrise les rouages de l’organisation. Sa position centrale lui confère une connaissance transversale et approfondie des enjeux et du fonctionnement de l’organisation. Son défi : conserver son impartialité en toutes circonstances.

L’objectif de l’audit externe est ciblé sur la situation financière de l’entreprise ou de l’administration, et le contrôle de ses comptes. Il permet de s’assurer de la conformité des états financiers avec les normes fiscales et comptables en vigueur.

D’une périodicité annuelle, la mission d’audit externe est exercée par un auditeur externe indépendant dans le cadre d’une mission à durée limitée.

Un audit externe peut aussi être commandé pour la certification d’une activité ou d’un système de management.

An effective internal audit relies on adherence to several good organizational and communication practices. To succeed in their mission, the auditor relies on:

Internal audit is an exercise constrained by international standards. As an exhaustive exercise, it involves many stakeholders and cross-references multiple data. Impeccable organization is essential to avoid getting lost in the numerous parallel tasks and to prevent any omission detrimental to the results.

With stakeholders: a neutral and impartial observer, the internal auditor must demonstrate open-mindedness. They build constructive dialogue, without succumbing to prejudices or interpretations, and without influencing the audited interlocutor.

To the changing context of the organization and external, regulatory, social, economic, or environmental developments.

Like many functions in business and the public sector, internal audit activity is affected by the digital revolution. Highly suited to internal audit, digitalization offers real productivity gains for the internal auditor. It facilitates cross-functional coordination, information sharing, and data collection. It frees the auditor from time-consuming tasks to refocus on their high-value-added activities: planning, analysis, and communication.

Digitalization also allows the auditor to devote more time to their monitoring mission. At the heart of transformations, internal audit activity is constantly confronted with new strategic and operational challenges. Continuous monitoring allows internal audit to adapt to changes, whether regulatory, economic, political, financial, environmental, or social.

Digitalization, combined with internal audit software, ensures the effectiveness of the internal audit mission. The result: a more efficient company, administration, or institution, closer to the needs of clients and users.

Values Associates has developed dedicated internal audit software for businesses and public sector entities.

Discover our software and request a demo.